Introduction

A bathroom remodel ranks among the most popular home improvement projects homeowners tackle—but the upfront cost stops many people before they ever pick up a tile sample. Most homeowners don't pay entirely out of pocket. Understanding your financing options before you commit puts you firmly in control of both the outcome and the budget.

This guide is written for homeowners in LA and Ventura Counties planning a bathroom remodel in 2026. Whether you're weighing a cosmetic refresh or a full gut renovation, you'll find every major financing route explained, a framework for choosing between them, and a pre-application checklist.

Key Takeaways:

- LA bathroom remodel costs range from $3,000 (cosmetic refresh) to $85,000+ (full gut renovation)

- Home equity loans and HELOCs typically offer the lowest rates for LA homeowners with significant equity

- LA midrange bathroom remodels recoup 89.6% at resale—among the strongest ROI of any renovation

- A detailed contractor quote before you apply anchors your loan amount and speeds approval

- Credit score, available equity, and debt-to-income ratio are the three factors lenders evaluate first

What Does a Bathroom Remodel Cost in 2026?

Before you approach a lender, you need a realistic number. Borrowing too much costs you in unnecessary interest; borrowing too little means scrambling mid-project.

The Three Cost Tiers

According to Angi's 2026 bathroom remodel data, costs break down across three broad scopes:

| Project Scope | Typical Cost Range |

|---|---|

| Cosmetic refresh (fixtures, finishes, no layout changes) | $3,000 – $10,000 |

| Midrange remodel (new tile, vanity, updated plumbing) | $10,000 – $25,000 |

| Full gut renovation (structural changes, custom features) | $25,000 – $80,000 |

The national average for a professional bathroom remodel sits at $12,141, though most projects with meaningful upgrades land well above that figure.

What LA and Ventura County Homeowners Actually Pay

Local labor and material costs run higher than national benchmarks. The 2025 JLC/Zonda Cost vs. Value Report puts the Los Angeles midrange bath remodel at $27,143 versus $26,138 nationally—and an upscale LA remodel at $85,055 versus $81,612 nationally. The gap isn't enormous, but it's consistent. It compounds further when you factor in LA County permit fees and the premium skilled tradespeople command in this market.

Get a detailed, itemized quote from a licensed local contractor—like Twin Oaks Construction, which serves LA and Ventura County homeowners—before you talk to any lender. That number, not a national average, should anchor your borrowing target.

Your Bathroom Remodel Financing Options

No single option is universally best. The right choice depends on your available equity, credit profile, how quickly you need funds, and how much risk you're comfortable carrying. Here's how each option works.

Home Equity Loan

A home equity loan gives you a lump sum at a fixed interest rate, repaid over a set term (typically 5 to 15 years). As of July 1, 2026, Bankrate reports the national average home equity loan rate at 8.09%, with a $30,000 10-year loan averaging 8.21%.

Best for: Projects with a clearly defined scope and a firm contractor quote in hand. The fixed rate means your monthly payment never changes, which makes budgeting straightforward.

Key trade-off: Your home serves as collateral. Missed payments carry real consequences. On the upside, interest may be tax-deductible when funds are used for home improvements—IRS Publication 936 confirms deductibility for funds used to buy, build, or substantially improve the home securing the loan. Consult a tax advisor to confirm your specific situation.

Home Equity Line of Credit (HELOC)

A HELOC functions like a revolving credit line secured by your home equity. You draw what you need during the draw period and repay only what you borrow. The national average HELOC rate as of July 1, 2026 was 7.46%—slightly below home equity loan rates.

Best for: Projects where the final cost is uncertain or work will happen in phases over time.

Watch out for: Variable-rate risk. If rates rise, your monthly payments increase with them. On closing costs, HELOCs often win—some lenders charge nothing upfront, which matters for mid-size projects where closing costs on a home equity loan would eat a meaningful percentage of the borrowed amount.

Cash-Out Refinance

Cash-out refinancing replaces your existing mortgage with a larger loan, and you pocket the difference. With 30-year fixed mortgage rates averaging 6.49% as of late June 2026 (per Freddie Mac), this only makes financial sense if the new rate is well below your current mortgage rate.

Best for: Large-scale projects where the cash-out amount justifies refinancing your entire balance. If you're sitting on a 3% mortgage from 2021, this option is hard to recommend.

Before proceeding: Ask your lender for a side-by-side comparison showing total interest paid over the life of the loan, both with and without the refinance. The math often surprises people.

Personal Loan

Personal loans are unsecured (no home as collateral), with fixed rates and a faster approval-to-funding timeline than any home equity product. Funding commonly arrives within 1 to 2 days. APRs for home improvement personal loans currently range from about 7% to 36%, with borrowers who have excellent credit averaging 14.21% as of July 2026.

Best for: Homeowners with limited equity, shorter repayment preferences (terms run 2–12 years), or those who want to keep their home out of the equation entirely.

Trade-off: Rates are higher than secured options, and the shorter terms mean larger monthly payments.

Credit Card Financing

Credit cards make sense in two scenarios: smaller-scope upgrades where you can pay off the balance quickly, or as a bridge while a larger loan processes. Current 0% introductory APR offers typically run 12 to 21 months, long enough to cover a cosmetic refresh if you're disciplined about payoff timing.

Avoid carrying a large remodel balance past the promotional period. Standard credit card APRs averaged 21.52% for accounts assessed interest in early 2026, far above any loan product. A high utilization rate can also drag down your credit score, affecting future borrowing capacity.

Cash / Savings

Paying cash means no interest, no lender approval, no collateral risk, and complete budget control.

Best for: Cosmetic or smaller projects where the out-of-pocket cost won't hollow out your emergency fund.

That said, a 0% promotional offer changes the calculus: keeping savings in a high-yield account while using interest-free financing may be the smarter move.

How to Choose the Right Financing Option

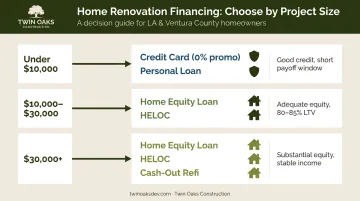

The right product depends heavily on project size and your financial position. Here's a practical starting framework:

| Project Size | Generally Best Fit | Condition |

|---|---|---|

| Under $10,000 | Credit card (0% promo) or personal loan | Good credit, short payoff window |

| $10,000 – $30,000 | Home equity loan or HELOC | Adequate equity (80–85% LTV after borrowing) |

| $30,000+ | Home equity loan, HELOC, or cash-out refi | Substantial equity; stable income |

The LA Equity Advantage

With the average LA home valued at $951,035 as of May 2026 (Zillow), many homeowners in this market have built substantial equity through years of appreciation. That equity makes home equity products especially accessible and lower-cost. For most LA and Ventura County homeowners with solid equity positions, a home equity loan or HELOC will offer better rates than any unsecured alternative.

Risk vs. Rate

Secured products (home equity loan, HELOC, cash-out refi) deliver lower rates but put your home on the line. Unsecured products (personal loans, credit cards) protect the home but cost more in interest. Before choosing a secured product, assess your income stability and current debt load. A low rate means little if a job change later puts your home at risk.

Matching Financing to ROI

The financing method should match the expected return. Financing a simple fixture swap with a 30-year cash-out refinance rarely makes financial sense. A home equity loan for a midrange remodel that adds lasting value—and that you'll live with for years—is a much more defensible choice. LA-specific data supports this: a midrange bathroom remodel in Los Angeles recoups 89.6% of its cost at resale, compared to 80% nationally.

One more option worth factoring into that ROI calculation: contractor-offered financing plans sometimes carry 0% promotional periods with no closing costs, which can outperform a personal loan for the right project and timeline.

What to Check Before You Apply

Lenders evaluating home equity products look at three things:

- Available equity — Most lenders require the combined loan-to-value ratio to stay at or below 80–85% after borrowing

- Credit score — Home equity loan lenders typically look for 680 or higher; personal loan lenders often accept scores starting at 600

- Debt-to-income ratio — Your total monthly debt payments relative to gross income; lenders typically prefer 43% or below

Knowing where you stand on all three before applying prevents surprises and speeds up the process.

Get Your Quote First

A detailed, itemized contractor quote anchors your borrowing amount to a real number and signals to lenders that you have a planned project, not a rough guess. Twin Oaks Construction offers free consultations where their team works through project scope and costs with homeowners—giving you a clear, accurate figure to bring into any financing conversation. You can start that process at twinoaksdev.com/contact or by calling (833) 621-7251.

That quote also tells you where to build in a cushion—because several costs catch homeowners off guard once work begins.

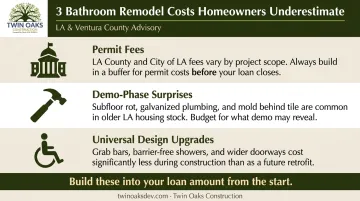

Costs Homeowners Commonly Underestimate

Build these into your financing amount from the start:

- Permit fees — LA County and City of LA both assess fees based on project scope; the LADBS e-Permit system calculates the exact amount at application, so build in a buffer from the start

- Demo-phase surprises — Subfloor rot, outdated galvanized plumbing, and mold behind tile are common in older LA housing stock; experienced local contractors can flag likely risks during the estimate phase

- Universal design upgrades — Grab bar blocking, barrier-free shower entries, and wider doorways cost far less to include during construction than to retrofit later; if you may need them eventually, include them now

Financing Your Bathroom Remodel in LA and Ventura County

High property values and years of appreciation have put many LA and Ventura County homeowners in a strong borrowing position. Combine that with the ROI data: a midrange bathroom remodel in Los Angeles returns 89.6% of its cost at resale according to the 2025 JLC/Zonda Cost vs. Value Report. For homeowners who plan to sell within a few years, the math on financing a quality remodel is genuinely compelling.

Twin Oaks Construction has spent over 20 years delivering bathroom remodels across LA and Ventura Counties. That regional experience matters in a market with specific permit requirements, older housing stock, and labor costs that diverge from national norms. Knowing local permit timelines and realistic labor costs means your estimate reflects what the project will actually cost — no surprises after you've already committed to a loan.

Before calling a lender, understand the true scope of your project. Request a consultation at twinoaksdev.com/contact and get an accurate estimate in hand before you discuss rates with anyone.

Frequently Asked Questions

Do people finance bathroom remodels?

Yes—financing is extremely common for mid-to-large bathroom projects. Home equity products and personal loans are the most popular methods. Most homeowners don't pay entirely out of pocket for remodels above $10,000.

What credit score do I need to qualify for a bathroom remodel loan?

Home equity loan lenders generally look for 680 or higher. Personal loan lenders often accept scores starting at 600, though lower scores mean higher rates. Checking your score before applying—and addressing any errors—takes minutes and can save thousands.

Is a home equity loan or personal loan better for a bathroom remodel?

Home equity loans offer lower rates but use your home as collateral; personal loans are faster and unsecured. If you have adequate equity and stable income, home equity usually wins on cost. Limited equity or a shorter payoff window? The personal loan is the practical choice.

How much equity do I need to finance a bathroom remodel?

Most lenders require the combined loan-to-value ratio to stay at or below 80–85% after borrowing. Given LA and Ventura County home values, many local homeowners have more borrowing room than they realize—worth calculating before assuming home equity products are out of reach.

Can I use a HELOC for a bathroom remodel?

A HELOC is one of the most popular tools for bathroom remodels—the draw-as-needed structure is ideal when costs are uncertain or the project unfolds in phases. The main risk: variable rates can increase your payment if rates rise during the draw period.

Are there government programs that help finance a bathroom remodel?

Several programs exist for accessibility upgrades and low-income homeowners. The FHA Title I program offers loans up to $25,000; veterans may qualify for the HISA grant ($6,800) or SAH grant (up to $126,526 for FY 2026). The LA County Development Authority also runs a Senior Grant Program and Handyworker Program—contact each directly to confirm current eligibility.